Last month, Zhongji Innolight announced its first-quarter report, with both revenue and net profit doubling. Its market cap broke through 1 trillion yuan, making it the second stock on the ChiNext board to achieve this after CATL.

Zhongji Innolight is the leading A-share optical module company, and also the primary party involved in the "old man buying liquor" incident:

In September last year, Ling Peng of Huangyuan Asset doubted that Zhongji Innolight's 2027 profit forecast of 25 billion only existed in an Excel spreadsheet. This prompted a golden-quote retweet from a Guosheng Securities telecom analyst: "Go buy your liquor, old man."

Since then, anything slightly related to liquor or real estate, or anyone talking about dividend payouts and margins of safety, has been uniformly slapped with the "old man" label.

After going viral, Zhongji Innolight proved its worth, with its market cap embarking on an astronomical surge. Following this quarterly report, combined with Eoptolink and TFC Communication breaking the 600 billion and 270 billion marks respectively, the A-share optical module trio's combined market cap exceeded that of Kweichow Moutai.

Wave after wave of AI data center construction has been the driving force behind the surging optical modules. Coupled with AI giants' capital expenditures far exceeding expectations, this超强行情 has been extended for several years, driving A-share optical modules completely crazy.

Amidst this fervent boom, Nvidia is quietly sharpening its knife.

The "Light" Connecting Computing Power

Before understanding what Jensen Huang wants to do, we must first explain the role and function of optical modules.

Behind every large model is a data center computing 24/7. Viewing the data center as a "computing factory," GPUs are the frontline workers responsible for the primary computing tasks.

However, the factory manager cannot directly command every worker. To make thousands of people work orderly and maximize efficiency, workers must be divided into groups and workshops. The role of optical modules is to connect the computing resources of the data center, allowing them to communicate and coordinate effectively.

Simply put, within a data center, there are three critical levels that require "communication":

The first level is the server. A server is a combination of several GPUs, equivalent to a "working group." Collaboration between GPUs requires communication interconnection, which is exactly what Nvidia's famous NVLink does.

A server composed of eight Nvidia GPUs

The second level is the cabinet, generally composed of multiple servers, equivalent to a "workshop." Each server must also coordinate and collaborate.

Placed together, these cabinets form the third level: the orderly "computing factory." Cabinets must also communicate with each other via switches.

A cabinet composed of servers

In a data center, both within levels (GPU to GPU, server to server) and between levels, interconnection is necessary to allow data to flow freely. If the flow takes too long, external computing tasks cannot enter, and calculated results cannot exit, dragging down overall computing efficiency.

The emergence of optical modules is precisely to solve the problem of transmission being too slow.

Over the past few decades, data center interconnection tasks were primarily completed by copper. The advantages of copper cables are zero power consumption, zero latency, and high reliability, without generating extra heat. Most importantly, it is cheap: Among all metals, copper's electrical conductivity is second only to silver, but its cost is far lower than silver.

Jensen Huang himself believes that as long as the physical distance allows, copper is the best connection method.

Inside Nvidia's GB200 NVL72 cabinet, 72 GPUs are connected by over 5,000 copper cables, with a combined length of up to 2 miles.

Copper cables inside the GB200 NVL72

However, as Huang noted, the biggest limitation of copper cables is physical distance: beyond 3-5 meters, the signal rapidly attenuates. Especially as the transmission distance between cabinets increases, the cables become as thick as an arm, making wiring very difficult.

About twenty years ago, Google tried using optical fiber to replace copper cables for communication between cabinets[4].

The biggest advantage of optical fiber/cable is its long transmission range. A standard single-mode fiber at 400G speed can transmit signals up to 10 kilometers with almost no loss, and power consumption for long-distance transmission is much lower.

The more troublesome issue is signal conversion.

Copper conducts electricity, so copper cables can directly transmit electrical signals sent by chips. However, optical cables are made of insulators like glass and plastic, requiring an extra "translator" installed—namely, the optical module.

When data enters the optical cable as an electrical signal, the optical module converts it into an optical signal; when the optical signal inputs into another device from the optical cable, the optical module converts it back into an electrical signal.

It can be said that wherever optical cables are needed, there is a demand for optical modules; the greater the demand for computing power and the lower the tolerance for data transmission latency, the higher the demand for optical modules.

In an Nvidia H100 computing cluster, an average of 6-8 optical modules are equipped per GPU, and the H200 cluster requires 18-24[5]. Optical modules have also iterated from 800G to 1.6T specifications.

But even so, Nvidia still feels it's not enough.

The CPO Revolution

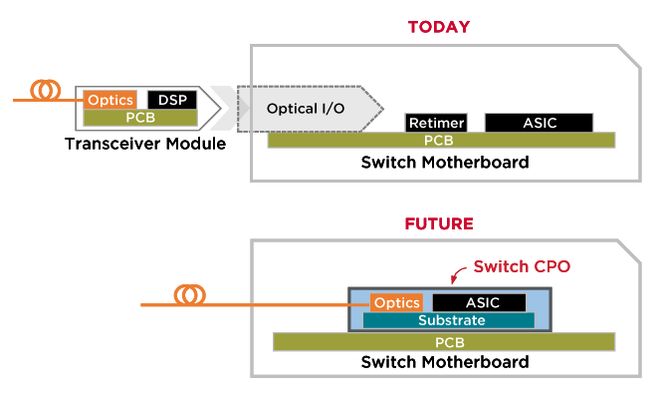

Nvidia's alternative is CPO (Co-Packaged Optics/Co-packaged Optoelectronics). As the name suggests, it involves installing the optical devices responsible for translation directly onto the electrical chips responsible for computing, cutting out the middleman.

The optical module itself is an assembly of various components. When Google initially explored replacing copper with fiber, the components responsible for translation were "loose." Later, as the industry matured and component specifications gradually standardized, they were "packaged" together to become modules.

After the rise of optical module manufacturers, optical modules became plug-and-play. A typical optical module is pluggable, inserted into a switch via a standard interface, and then connected to the optical cable. The electro-optical signal conversion is completed the moment data passes through the optical module.

Pluggable optical module

However, the larger the data center scale, the greater the demand for optical modules, which brings a problem: power consumption.

The faster the data transmission, the higher the power consumption. The power consumption of the latest 1.6T optical modules has surged from 1W in the 10G era to 30W. At the beginning of the year, Nvidia complained at GTC that optical interconnect power consumption already accounts for 10% of the total power consumption of the computing system.

A large part of the optical module's power consumption is spent "on the road":

When the signal "travels" from the switch to the optical engine inside the optical module, signal loss occurs. To compensate for this loss, the DSP inside the optical module is needed; the more compensation required, the higher the power consumption.

Nvidia's idea is simple: since the road is too long, shorten it:

The electrical chip speaks English, and every data transmission requires the optical module to check a dictionary and translate it into Chinese. Why not just stuff the dictionary directly into the electrical chip and let it translate and output Chinese directly? This is the concept of CPO—breaking the optical module apart again.

According to Nvidia's vision, core components like the optical engine can be taken out of the optical module and placed next to the switch chip, saving the cost of hiring a translator.

Traditional optical module (above) vs CPO (below)

Of course, if it were just for that little power consumption, one would be underestimating Mr. Huang. Huang argued years ago that if it only sold chips, Nvidia certainly wouldn't be worth this much money. Therefore, Nvidia "is definitely not a chip company," but rather aims to sell the entire "computing system."

To realize this grand vision, Nvidia still needs an ally: TSMC.

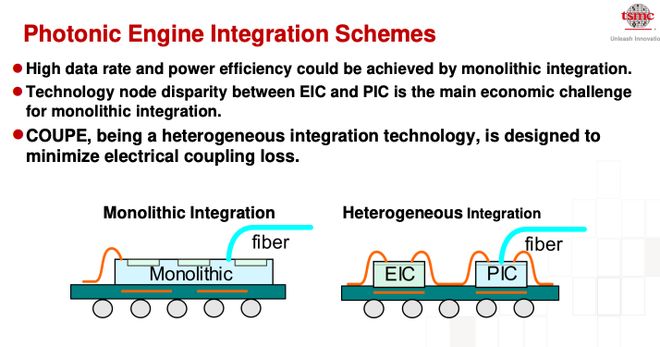

The technical concept of CPO is to "stick" optical devices onto electrical chips, which requires advanced packaging technology. TSMC happens to be the company with the earliest layout, largest investment, and most R&D achievements in the field of advanced packaging.

At the 2021 Hot Chips conference, TSMC showcased COUPE (i.e., CPO) technology on a PPT for the first time. Subsequently, industry rumors emerged that Nvidia was planning a silicon photonics integration R&D project, with TSMC as a key member.

COUPE technology showcased in TSMC's 2021 Hot Chips PPT

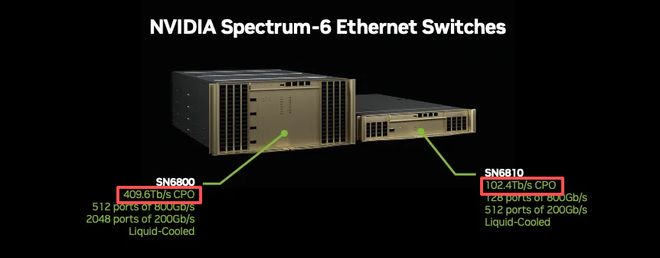

The latest result of this good alliance's collaboration is the Vera Rubin NVL576 AI supercomputing platform released earlier this year.

The Spcectrim-SPX switch cluster responsible for inter-rack communication utilizes CPO technology, placing the optical engine right next to the switch chip. By removing third-party optical modules, Nvidia's control over the entire system is unprecedented.

Nvidia's Spcectrim-SPX switch

Jensen Huang stated that switching from optical modules to CPO, "the 6 megawatts of power saved is equivalent to the power consumption of 10 Rubin Ultra racks."

According to Nvidia's roadmap, integrating the optical engine with the switch chip is only the beginning; the ultimate goal is to integrate the optical engine into the GPU, with the mass production node tentatively set for 2028.

Meanwhile, at the recent SEMI Forum, TSMC also announced that its COUPE platform is expected to officially enter the mass production stage in late 2026[6], meaning: COUPE is ready to start taking large-scale orders.

Two tech fanatics are sharpening their knives, seemingly about to completely wash away the long-standing landscape of optical modules.

Eliminating the Middleman

Nvidia breaking the optical module apart and remaking it will directly strike system integrators.

This segment happens to be the one where Chinese companies are most dominant in the entire optical module industry chain. Zhongji Innolight and Eoptolink rank first and third globally in optical module shipments, and seven of the global top ten are Chinese companies (2024).

Optical module integration belongs to precision manufacturing. The biggest technical challenge is alignment accuracy, ensuring optical signals dock between various components with minimal loss. Alignment accuracy usually needs to be controlled at the μm level, and the higher the speed, the greater the number of channels.

For the latest 1.6T optical modules, the placement accuracy for optical chips must reach ±3μm, and for electrical chips, ±10μm[9].

Zhongji Innolight holds a 70% market share in 1.6T optical modules and is one of Nvidia's core suppliers. Its first-quarter gross margin was 42.61%, reaching ceiling levels compared to the industry average of under 20%.

However, from the perspective of the upstream and downstream structure, system integration still belongs to the downstream assembly segment.

In other words, when Nvidia uses CPO to dismantle optical modules, it is dismantling the parts Chinese companies excel at. In the remaining optical devices and electrical chips, Chinese manufacturers have a thin presence.

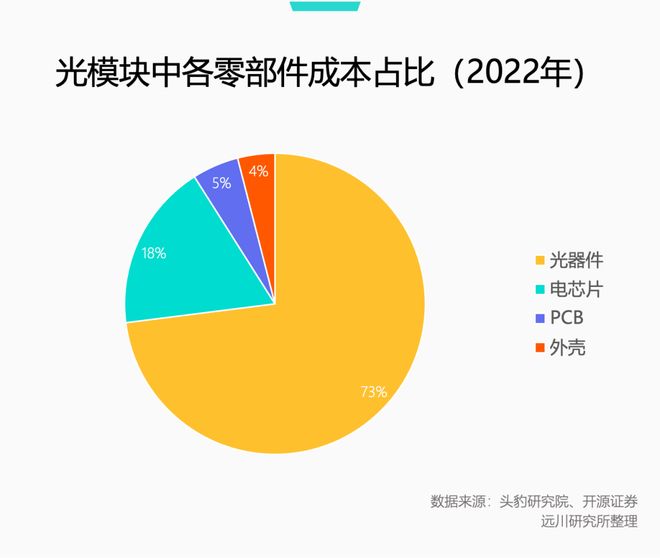

Among optical devices, lasers and detectors are key to the "translation" function. Optical devices account for over 70% of the cost of an optical module, and lasers and detectors together account for over 50% of the cost of optical devices.

Electrical chips account for nearly 20% of the optical module cost, with core components being DSP chips and AFE analog front ends, used to ensure the accuracy of "translation."

These four major components in the two categories are currently completely monopolized by US and Japanese manufacturers. Especially in high-end products, Chinese manufacturers have almost no presence.

High-end lasers are firmly controlled by Lumentum, Coherent, and Broadcom (USA), as well as Mitsubishi and Sumitomo Electric (Japan); detectors are dominated by four giants: GCS, SiFotonics, Coherent, and Broadcom.

Although China's domestic Source Technology has shipped high-end lasers, most other manufacturers are stuck in the low-end market.

DSPs and AFEs are typical analog chips, which are the traditional forte of analog chip veteran artists like Broadcom, Marvell, and MACOM in the US; Chinese manufacturers are even more marginalized here.

Domestic optical module companies mostly purchase core components from US and Japanese manufacturers, then package them into optical modules. Although gross margins are good, this hasn't changed their positioning as "middlemen" in the optical module industry.

Judging from Nvidia's moves, it is already preparing for the removal of optical modules from the table.

Just in the first quarter of this year, Nvidia successively made strategic investments of 2 billion USD each in Lumentum and Coherent, both of which are current global leaders in high-end lasers. These two investments directly locked down laser capacity for the next few years.

Upstream manufacturers are also holding the emperor hostage to command the nobles, leveraging their technological advantages to replace optical module manufacturers and become tier 1 suppliers themselves.

For example, Broadcom, which dominates high-end DSPs, is another ally of TSMC's COUPE technology besides Nvidia, and was the earliest manufacturer globally to commercialize CPO, having released related CPO products in 2024.

Once this trend of major customers and upstream suppliers squeezing integrators together forms, life will become very difficult for the integrators.

The good news is that, given the high costs and complex technology, CPO will likely only be applied to a few high-end switches in the short term. Meanwhile, most mid-to-low-end and high-end scenarios will be enough to keep optical module manufacturers from worrying about orders for the next few years.

But considering that these Silicon Valley folks are already talking about launching data centers into space, using CPO to eliminate optical modules doesn't sound so far-fetched anymore.

Source: Yuanchuan Technology Review

微信扫一扫打赏

微信扫一扫打赏  支付宝扫一扫打赏

支付宝扫一扫打赏

Comments (0)