For the fiscal year ending March 2026, Japanese automakers collectively delivered their worst annual reports. The overall picture was strikingly consistent, though each company faced its own unique hardships.

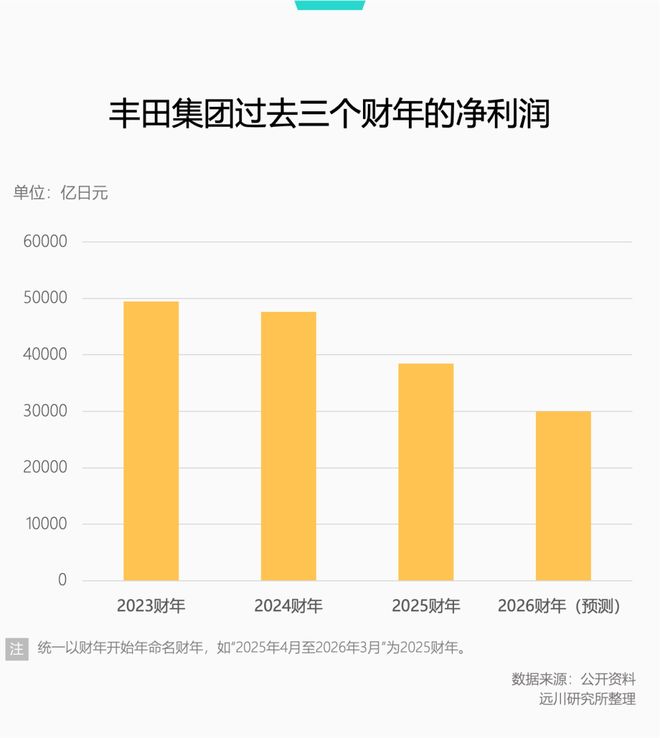

Industry leader Toyota saw its net profit decrease by 38.7 billion yuan (RMB, same hereinafter) year-on-year, with the main culprit being US tariffs. However, Toyota is a massive enterprise after all, with a net profit of 163.5 billion yuan remaining, more than five times that of BYD.

In comparison, the smaller players each have their own struggles.

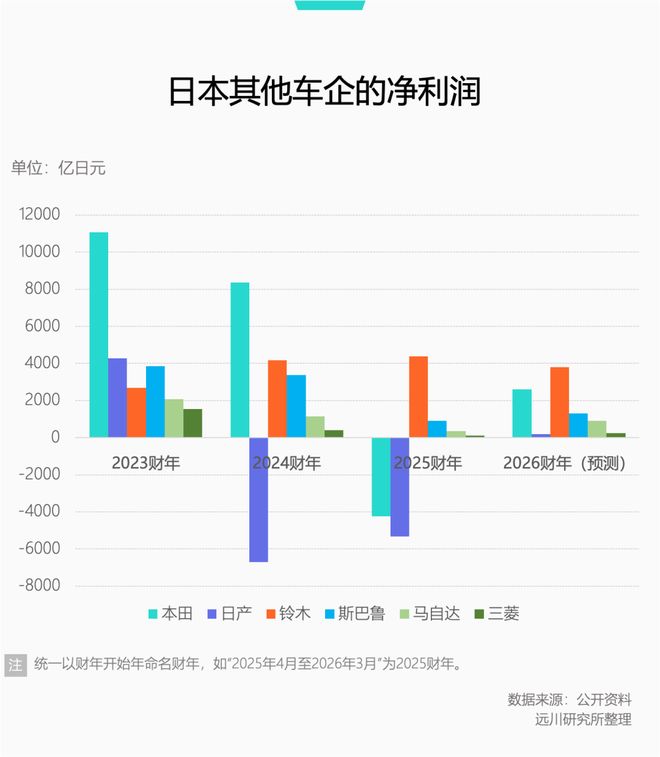

Honda restructured its EV business, halting three EV projects nearing mass production. All R&D and tooling costs went down the drain, and the Afeela model developed with Sony also fell through. A one-time impairment of 55.7 billion yuan was recorded, directly causing a full-year swing from profit to loss, with a net loss of 18 billion yuan.

Nissan's situation is even worse, with losses for two consecutive years. Factory closures and layoffs generated billions in restructuring costs, causing its profitability to plummet to third-tier status.

With poor performance in the old fiscal year, the guidance for the new fiscal year is also bleak.

According to the fiscal 2026 (March 2026 - March 2027) guidance provided by the seven major automakers (Toyota, Honda, Nissan, Suzuki, Mazda, Subaru, Mitsubishi), their combined net profit is only 167.5 billion yuan, just 4 billion yuan more than Toyota's net profit alone last year, and a full 152.5 billion yuan less than the peak of Japanese cars in 2023.

Looking back at 2023, Japanese automakers' profits hit record highs one after another, with Toyota's 210.1 billion yuan net profit refreshing the record for Japanese manufacturing enterprises [1].

Who could have imagined that this was likely the best year Japanese automakers would see in the next decade?

Neither the East nor the West is shining

Regarding Japanese cars, there has long been a narrative: Japanese cars are struggling in China, but flourishing overseas.

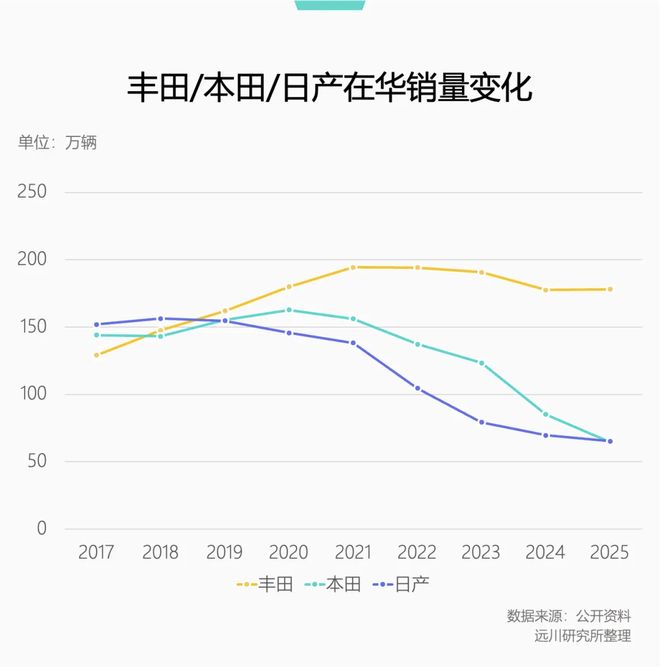

This is indeed true for the Chinese market. In 2020, Japanese cars held a 24.1% share in China, but by the first quarter of this year, it had shrunk to 13.8%.

The overall share shrank by 10%, but Toyota actually only suffered superficial wounds, with relatively high profit pressure. The ones truly badly hurt are mainly Honda and Nissan, whose sales have been cut in half.

In January this year, Honda's iconic Fit model had a generational update in China, with a limited release of 3,000 units. Unexpectedly, in a vast nation of 1.4 billion people, only 3,000 people who truly understand cars could be found.

The failure in the Chinese market can be explained by the high penetration rate of electric vehicles, but if we break down the overseas markets, we find that the foundation of Japanese cars is not that solid.

Japanese cars' overseas markets can be divided into two major blocks:

First, markets where Chinese cars are difficult to enter or cannot enter at all, such as India and the United States, where Japanese car sales are doing well.

The leader in India's passenger car market is Suzuki, which held a 51% market share at its peak. Although it has declined in recent years, it still maintains over 40%. The Indian market is characterized by a large base but low volume; even in a good year, Toyota can only sell over 300,000 vehicles.

The United States is the largest single market for many Japanese automakers. Last year, Japanese automakers sold 6 million new cars in the US, and Toyota's appeal is second only to the domestic giant GM [2]. Although the US raised tariffs on imported Japanese cars to 15%, the main damage was to profits.

Second, in markets where Chinese automakers are aggressively attacking, Japanese cars have actually taken a significant hit.

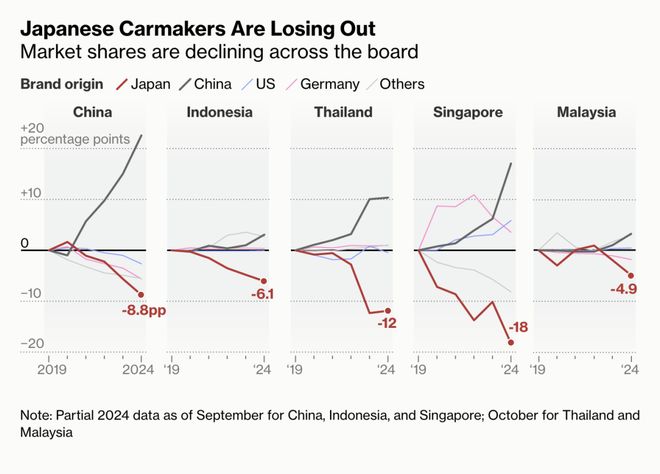

First is Southeast Asia, where Japanese cars have been entrenched for over 60 years, with a long-term market share above 80%. Especially in Thailand and Indonesia, Japanese cars previously held over 90% of the share, wielding absolute dominance.

However, after Chinese automakers entered Southeast Asia, they directly squeezed out Japanese cars' share. According to Bloomberg statistics [3], from 2019 to 2024, the share of Japanese cars decreased by 6% in Indonesia, 12% in Thailand, and 18% in Singapore.

At the same time, in these markets with low trade barriers against China, while Japanese cars have a solid base, domestic automakers are growing very fast. We can compare the industry leaders BYD and Toyota:

Indonesia: In 2023, Toyota sold 336,000 vehicles, BYD 0; in 2025, Toyota 250,000, BYD 46,000 [4].

Thailand: In 2023, Toyota 276,000, BYD 29,000; in 2025, Toyota 230,000, BYD 40,000 [5].

Brazil: In 2023, Toyota 192,000, BYD 17,000; in 2025, Toyota 163,000, BYD 113,000.

UK: In 2023, Toyota 109,000, BYD 0; in 2025, Toyota 90,000, BYD 51,000.

Comparing other automakers also shows the trend of "Japan standing still while China grows rapidly":

Indonesia: In 2023, Honda 139,000, Chery 4,000; in 2025, Honda 56,000, Chery 19,000.

Australia: In 2023, Nissan 39,000, Geely 0; in 2025, Nissan 35,000, Geely sold 5,000 in its first year entering Australia.

This is still a comparison across all energy types; if we look solely at new energy vehicles, the gap is even more astonishing.

In other words, the current survival status of Japanese automakers cannot be simply explained by the China/overseas framework. The more direct cause must be found in the energy structure.

Hybrids are a double-edged sword

The relatively stable markets for Japanese cars mostly share one characteristic: Hybrid vehicles (HEV) are still going strong.

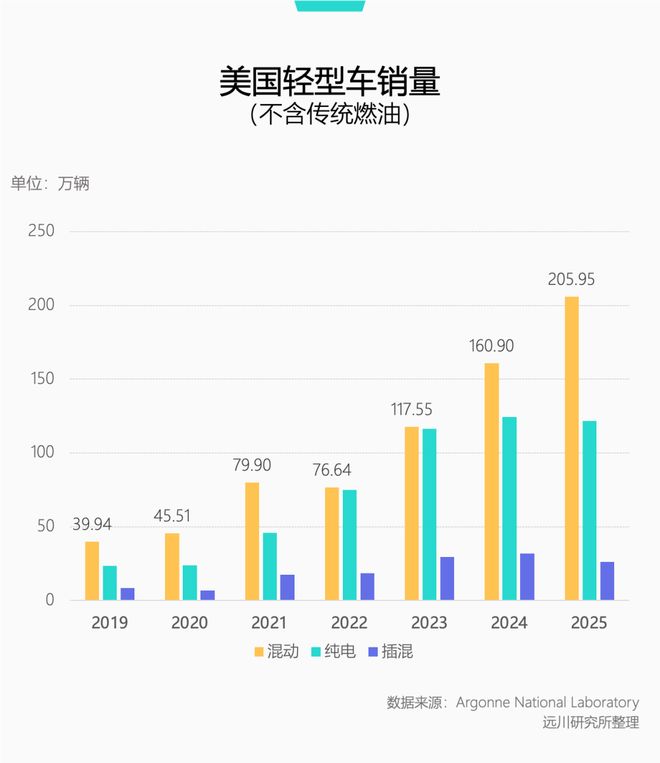

The most typical example is the United States. By energy type, hybrids have consistently been the second largest market after internal combustion engine vehicles. On the contrary, pure electric vehicles have shown insufficient growth momentum after 2023, while the growth momentum of hybrids has not stopped to this day.

According to S&P Global data, this March, the share of hybrid vehicles in the US increased to 15.3%. From the end of February to April, US hybrid vehicle sales continued to surge by 37%, outpacing the overall auto market growth of 15% [6].

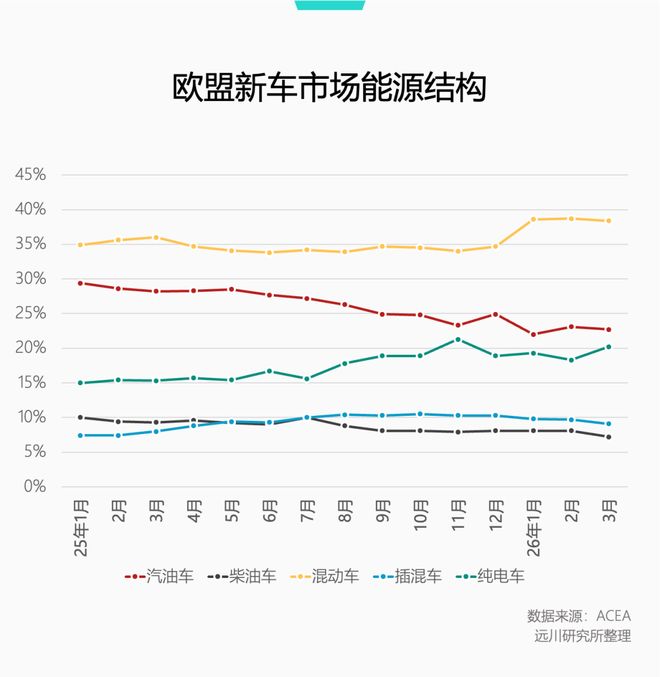

The situation in the EU market is similar. Over the past year, the EU's internal combustion engine vehicle share shrank by nearly 10%, but pure electric penetration only increased by 5%, with the remaining share basically siphoned by hybrid vehicles.

Although the EU talks about electrification transition every day, infrastructure construction is seriously insufficient. From 2017 to 2023, EU pure electric vehicle sales grew 18 times, but charging piles only grew 6 times. Even in regions with better infrastructure, fast charging piles are severely lacking.

In addition, in many parts of Europe, you have to bring your own charging cable (usually given with new cars), because people often use professional hydraulic cutters to steal cables. Weak infrastructure and tough civil conditions inevitably make consumers hesitate to embrace energy conservation and emission reduction.

The cut is clean and neat, the technique is professional and exquisite

By the first quarter of this year, the share of hybrid vehicles in the EU reached 38.6%, supporting Toyota's annual sales of 1.2 million in the EU.

Japanese automakers have suffered repeated defeats on the pure electric track, but in the hybrid field, they are virtually unrivaled. This track was defined by the Japanese, followed by the Koreans, ignored by Europe and the US, and only began to be studied by Chinese automakers in recent years.

Among them, Toyota's THS (Toyota Hybrid System) was first installed in the Prius and has now developed to the fifth generation, establishing Toyota's dominant position in hybrid technology, with a long-term market share around 40%.

Honda's i-MMD (now called e:HEV) had a slightly bumpier journey, but with its electric-centric design logic, balancing low fuel consumption and the smoothness of electric cars, it rose rapidly. In the US, the CR-V can sell 400,000 units a year thanks to its hybrid version.

Because Nissan focused on pure electricity early on and did not launch hybrid products in time, it missed the early window of the hybrid explosion. It wasn't until 2016 that it mass-produced the e-POWER hybrid system, and it is now racing to catch up and supplement its hybrid lineup.

In other words, what truly determines the survival status of Japanese automakers is the degree of acceptance of hybrids in different markets. Once demand shifts, a crisis follows.

Last November, Toyota released the new generation Hilux pickup at the Bangkok International Motor Show, a carefully chosen location. The Hilux is Thailand's national iconic vehicle and hadn't been updated for ten years. What's intriguing is that Toyota took the opportunity of this update to rarely add a pure electric version.

Toyota's explanation was "to provide consumers with more choices," but the real reason is likely that the hybrid market in Thailand and even Southeast Asia is shrinking, and Chinese new energy vehicles are eyeing the territory covetously.

Last year, the new energy penetration rates in Thailand and Indonesia increased to 23% and 13% respectively. This April, Thailand's pure electric vehicle penetration rate broke through 23%, already very close to the share of hybrids. If the pure electric offensive continues, the territory Japanese cars have built over decades will have to be handed over.

A similar situation is also playing out in markets like Brazil and Australia. Brazil's electric vehicle share is not high, only in the single digits, but growth is significant. Chinese automakers ship 50,000 electric vehicles to Brazil every month, continuously squeezing the living space of Japanese cars.

Under these circumstances, Japanese automakers have made a tacit and consistent choice: shrink their electric vehicle business and focus R&D on internal combustion and hybrid vehicles. Rather than risking extending the R&D battle line, it's better to further strengthen their own strengths.

In Toyota's sales targets, it plans to produce 6.7 million hybrid and plug-in hybrid vehicles by 2028, implying that the lifecycle of hybrid models is still very long.

If the future global auto market landscape turns out as Akio Toyoda predicted, where hybrids, internal combustion, and pure electrics will coexist for a long time in a three-way split, then with no progress in pure electric R&D, actively shrinking to focus on traditional advantageous sectors is indeed a very pragmatic business decision.

It's just that those profits taken away by electrification will never return.

微信扫一扫打赏

微信扫一扫打赏  支付宝扫一扫打赏

支付宝扫一扫打赏

Comments (0)