Are high-speed rail fare hikes starting again?

01

Even the most profitable high-speed rail is raising its prices.

Recently, the Beijing-Shanghai High-Speed Railway Company announced a 20% increase in the published ticket prices for some train services on the Beijing-Shanghai high-speed line and the Hefei-Bengbu high-speed line.

This is not the first time high-speed rail has raised prices.

As early as two years ago, four high-speed rail lines, including the Wuhan-Guangzhou, Shanghai-Hangzhou, Shanghai-Kunming, and Hangzhou-Ningbo passenger dedicated lines, collectively raised their fares, with some routes seeing increases of nearly 20%.

High-speed rail price hikes are not new, and a wave of utility price increases has long arrived, but the surprise is that this time, the one raising prices happens to be the most profitable high-speed rail.

As is well known, among the hundreds of high-speed rail lines nationwide, only a few—such as Beijing-Shanghai, Guangzhou-Shenzhen-Hong Kong, Beijing-Tianjin, Shanghai-Nanjing, Shanghai-Hangzhou, and Nanjing-Hangzhou—can achieve stable profitability.

The Beijing-Shanghai high-speed rail is the most profitable among them.

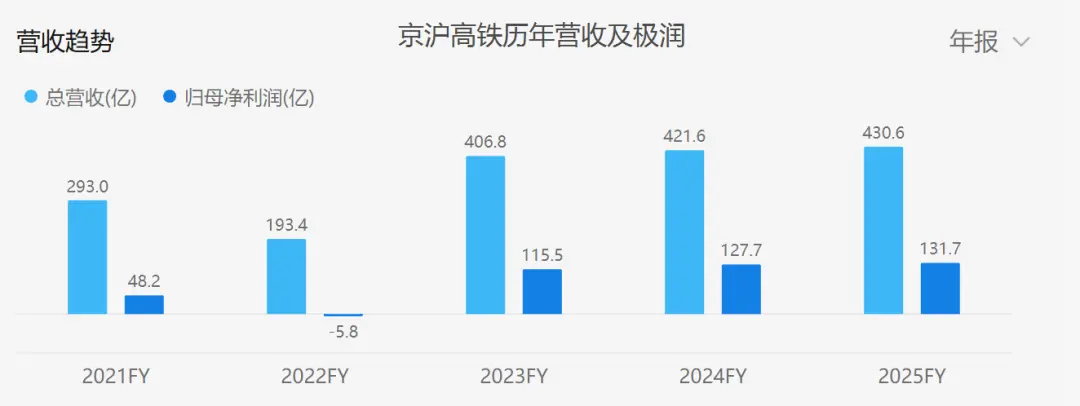

In 2025, the Beijing-Shanghai High-Speed Railway achieved an operating revenue of 43.062 billion yuan and a net profit attributable to the parent company of 13.172 billion yuan.

Since its listing, except for the relatively unusual year of 2022, the Beijing-Shanghai high-speed rail has been profitable almost every year, earning it the title of China's most profitable high-speed rail.

Behind its profitability is the strong support of massive passenger traffic.

The Beijing-Shanghai high-speed rail line connects Beijing and Shanghai, linking the two major city clusters of Beijing-Tianjin-Hebei and the Yangtze River Delta. The regions it passes through are all major economic and demographic provinces.

As the route with the most trains, the highest passenger density, and the highest occupancy rate in the world, the Beijing-Shanghai high-speed rail runs a train every 3 minutes during peak times, a frequency comparable to a subway.

Last year, the Beijing-Shanghai high-speed rail sent a total of 238 million passengers, averaging 650,000 per day.

Workers working along the way are often seen on the trains, earning the Beijing-Shanghai high-speed rail the nickname of "China's high-speed rail with the strongest work vibe."

Even so, tickets remain hard to get during holidays, and with the "transit" demand from a large number of cross-line trains, capacity becomes even tighter.

Therefore, a second Beijing-Shanghai high-speed rail has been put on the agenda, connecting Beijing and Shanghai via Shandong and Jiangsu, but it won't be fully operational until around 2028.

In the short term, the demand for passenger traffic on the Beijing-Shanghai high-speed rail exceeds supply, which has become the core reason why the most profitable high-speed rail dares to raise prices.

Since the beginning of this year, geopolitical conflicts in the Middle East have intensified, crude oil prices have soared, and the civil aviation market has raised prices accordingly. This highlights the cost-effectiveness of high-speed rail, making fare hikes seem even more justified.

02

Why do high-speed rail fares keep increasing?

High-speed rail has seen multiple rounds of price hikes, and even the most profitable line is no exception. What does this indicate?

As the world's largest high-speed rail country, China's "Eight Vertical and Eight Horizontal" high-speed rail network has largely taken shape, with over 50,000 kilometers of lines covering 97% of cities with an urban population of over 500,000.

Currently, 12 provinces nationwide have achieved "high-speed rail access to every city," including those in the western regions like Guizhou and Guangxi, and Liaoning in the northeast.

However, high-speed rail construction is expensive, and the return on investment cycle is relatively long.

Investment requires money, operations require money, and later maintenance also requires money. Where does the money come from?

Fortunately, under the national coordinated strategy, during the era of massive infrastructure construction, transfer payments from the eastern regions and the issuance of various local bonds were enough to solve the initial funding problems, allowing less developed areas to quickly join the high-speed rail network.

However, any large-scale, forward-looking construction requires the premise of strong economic, fiscal, and demographic growth. Without passenger traffic as support, most lines lack economic viability.

In fact, there are only a few high-speed rail lines in China that can achieve stable profitability.

When the economy is booming, none of this is a problem.

If the logic reverses, high-speed rail price hikes become an inevitable event. The deeper a line falls into loss, the stronger the impulse to adjust prices.

This logic is consistent with highways attempting to extend their toll collection periods.

Not long ago, several highways announced the end of toll collection upon expiration, but some continued to extend tolls under the name of renovation and expansion, and even some national highways restarted toll collection.

High-speed rail does not have a toll collection deadline, and the lines possess a certain monopoly characteristic. As long as they want to raise prices, there is hardly much resistance.

Moreover, since the beginning of this year, geopolitical conflicts have intensified, prices of bulk commodities like crude oil have soared, inflation has begun to transmit, and there is widespread upward pressure on prices.

It's not just high-speed rail; even subways, tap water, and gas are seeking price increases.

03

Not all high-speed rail lines have the capital to raise prices.

Have you noticed that the high-speed rails in these two rounds of price hikes are basically in developed regions, mostly lines that can make a profit?

This phenomenon is not accidental. Faced with mounting debt and operational pressures, no high-speed rail wouldn't want to raise prices, but it's not something that can be done just by wanting to.

This is not about price controls. As early as 10 years ago, high-speed rail had already liberalized market-oriented pricing. In recent years, flexible pricing has become prevalent, implementing differentiated discount floating strategies with both increases and decreases.

The problem is that passenger traffic is the biggest constraint. If the daily occupancy rate is extremely low, wanting to raise prices won't be of much use.

Some lines have a massive shortfall in passenger traffic; once prices are raised, passenger flow will only continue to shrink, which also limits the ability of loss-making lines to raise prices.

This is only the first constraint; the other constraint lies in the fierce competition between high-speed rail and civil aviation.

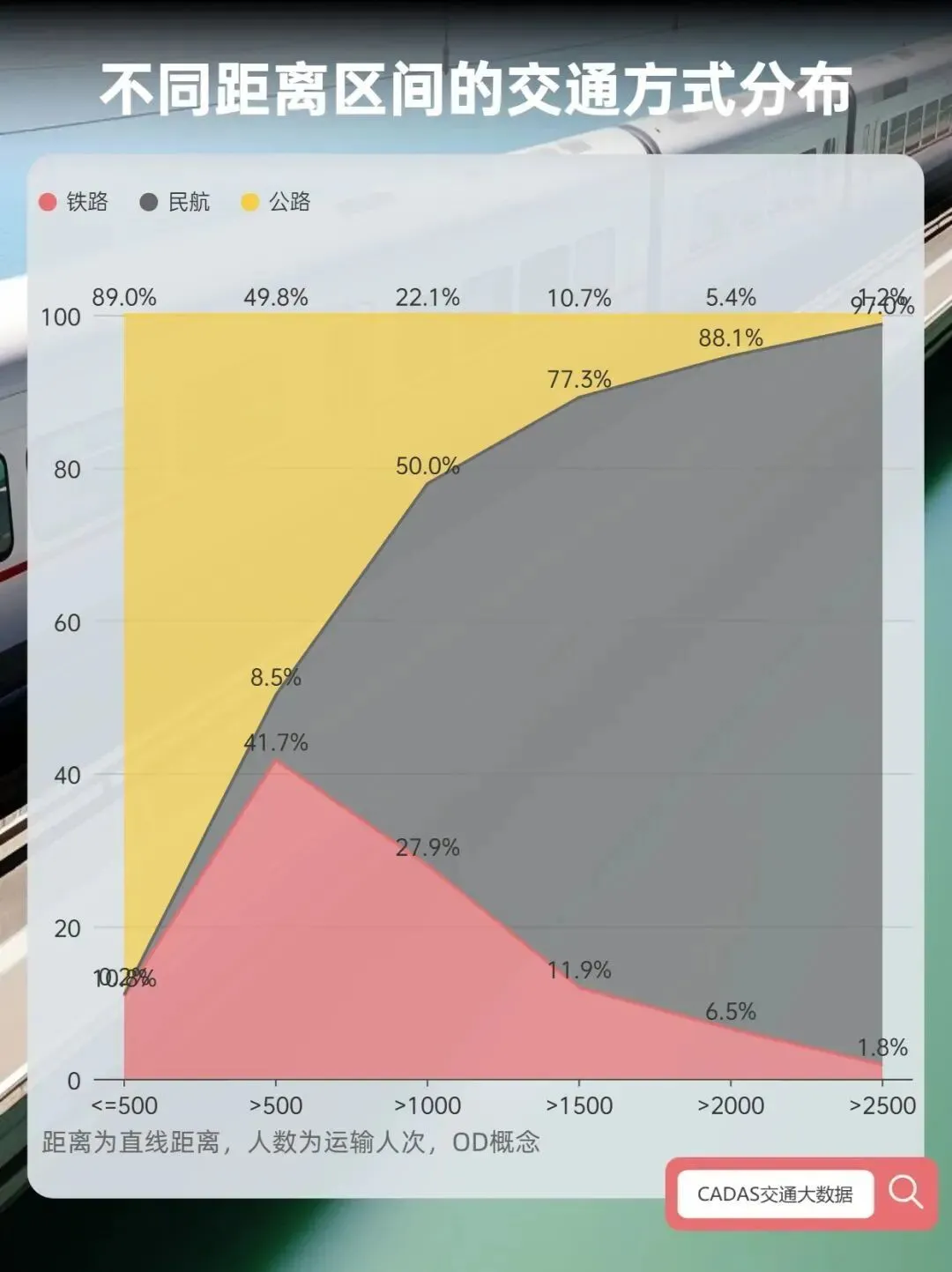

Generally speaking, within 800 kilometers, the cost-effectiveness of high-speed rail stands out; above 1,200 kilometers is the advantageous zone for civil aviation; between the two, there is intense competition.

This is precisely why airports in Wuhan, Changsha, and Zhengzhou have relatively low passenger throughput. High-speed rail extends in all directions, squeezing civil aviation.

High-speed rail "squeezes" civil aviation, but civil aviation also "squeezes" high-speed rail.

When civil aviation raises prices due to surging international oil prices, the cost-effectiveness of high-speed rail becomes prominent; when high-speed rail continuously raises prices, the attractiveness of civil aviation will return.

In fact, there is inherent tension between the public attribute and the market attribute of high-speed rail. In the face of debt pressure, the former will likely have to yield to the latter.

Moreover, promoting a reasonable rebound in prices is inherently a policy goal, superimposed with the pressure of imported inflation and the realistic demand for price hikes driven by debt burdens.

From high-speed rail to subways, and then to water, electricity, and gas, the emergence of a wave of utility price hikes is highly probable.

To put it in the same old saying: if housing prices don't rise, everything else will start to rise.

Source: WeChat Official Account: National Strategy, Author: Kaifeng

微信扫一扫打赏

微信扫一扫打赏  支付宝扫一扫打赏

支付宝扫一扫打赏

Comments (0)