Li Ming, a post-00s young man, is the "kid from another family" in the eyes of his old classmates. He was studying his dream psychology major at a key university and even planned to pursue a PhD. Every time he went to relatives' houses for dinner with his parents, the relatives would praise him for being excellent. His mother would politely say, "Not at all," but he could feel that she was always proud of him.

However, no one knew that he was carrying 160,000 yuan in online loans—owed to Du Xiaoman, Meituan Borrow, and Didi's Di Shui Dai.

Such stories are not rare on the internet. But what we are going to talk about is not just a story of a young man sinking into online loans.

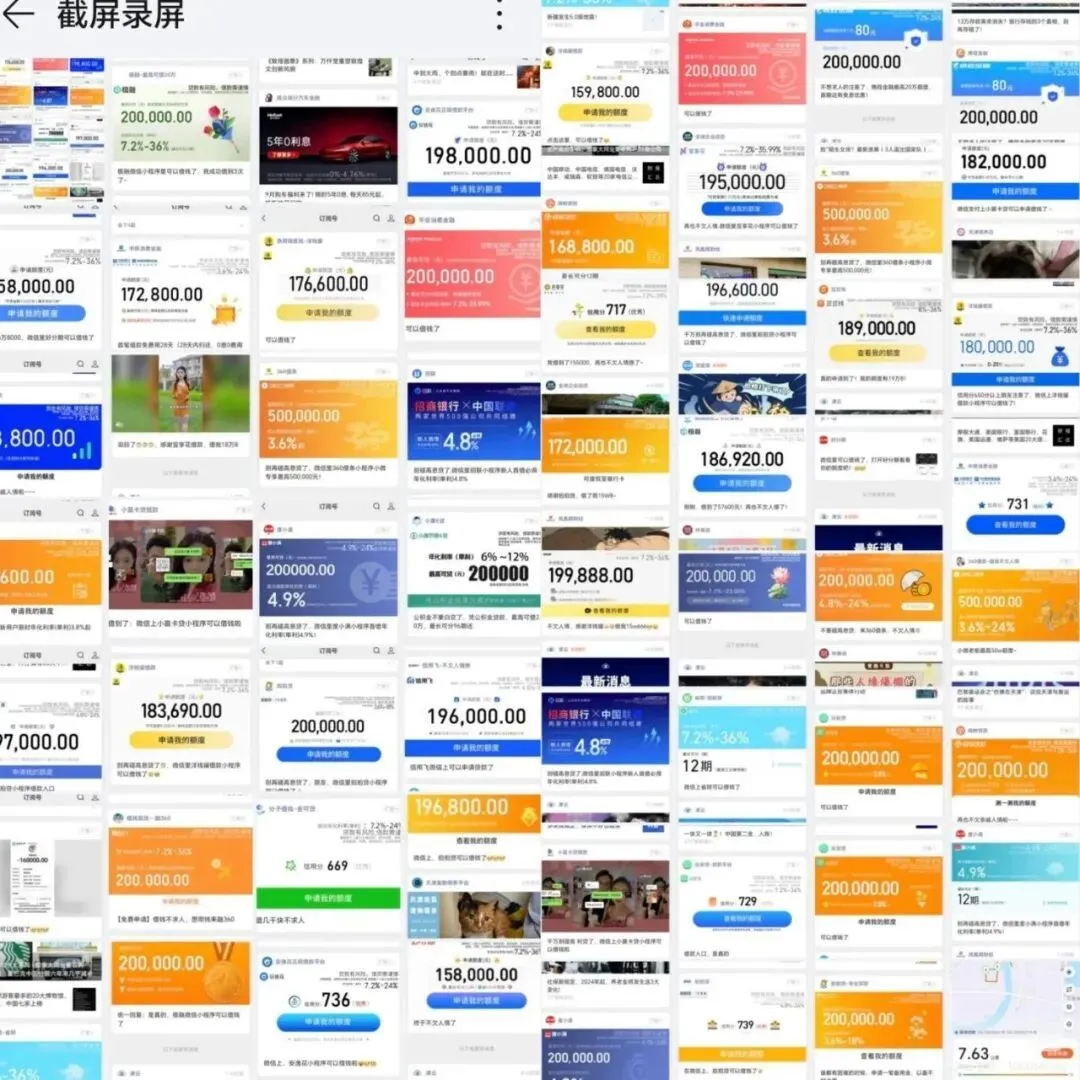

In Li Ming's phone, "bait" is everywhere. From "buy now, pay later" to "default Baitiao or monthly payment," and "coupon-driven traffic," major apps hide online loan entrances in daily scenarios. Behind them, the giants have already divided up the territory: according to iResearch, Ant, ByteDance, JD, Du Xiaoman, and Meituan monopolized nearly 80% of the internet lending market in 2024.

In this massive net stand young people moving forward under the weight of debt. Nielsen once surveyed that the credit penetration rate among Chinese young people reached 86.6%. Among them, internet installment products, with a usage rate of 60.9%, far exceeded credit cards' 45.5%, becoming the first choice for young people. Many Chinese young people first encounter credit consumption on the payment pages of daily apps for shopping, food delivery, ride-hailing, and short videos.

Even though he was well-versed in psychology, Li Ming underestimated the power of this system. It has undergone rigorous legal review, wearing the cloak of compliance; the loan interest rate does not exceed the 24% annualized red line, the agreements seem transparent, and even the advertisements appear "tender," with posters saying "Accompanying you to a happy start." It permeates every aspect of life like air, accurately capturing every impulse to consume, making it hard to break free.

How exactly is all this achieved? Phoenix Net contacted 8 online loan product designers, 6 from tech giants and 2 from leading online loan companies. They meticulously decoded a world of internet lending that legally "hunts" human nature and "tailors" to desire.

When borrowing money has become an "addiction," people like Li Ming can no longer distinguish which primal desires originate from themselves and which are merely carefully fed conditioned reflexes.

"Why not give it a try?" Li Ming's curiosity and the urgency of needing money finally overpowered his reason.

The loan process was smoother than he had imagined: fill in his name, upload the front and back of his ID card, undergo facial recognition, and agree to pull his credit report. Only when filling in his income did he pause, selecting the "2,000-3,000 yuan" option based on his living expenses.

In less than a minute, the screen flashed, the loan limit was issued, and he was given 43,500 yuan.

His tense nerves instantly relaxed, and this huge number made him feel pleasantly surprised. He had only heard the word "loan" from his parents or in TV dramas before, always feeling it was a "big deal" that required collateral and involved large amounts, easily a hundred thousand at a time. Now, almost without any conditions, as long as you click a button, it tells you: it can give you this much money.

Whenever the repayment date approaches, anxiety always drags Li Ming back to that afternoon.

It was an afternoon in May 2023, during his senior year graduation season, and the air was filled with a restless energy. Gatherings, farewell trips—within less than half a month, Li Ming had spent his two thousand yuan living expenses. He had already blushed and asked his family for a thousand yuan, barely scraping by until the end of the month. Just then, a classmate sent an invitation: want to go to a music festival? Tickets are 400 yuan. "I don't have money"—these three words got stuck in his young, proud throat, unspoken.

The dorm was extremely quiet; he was the only one there, and his eyes fell on the line of text on his phone screen: "Check Limit."

Two or three months earlier, he had casually opened the Baidu App, and the "Du Xiaoman" lending ad on the splash screen flashed by. Now, he opened Baidu again out of boredom, and in the "My" section at the bottom right of the App, he saw "Du Xiaoman," and a thought awakened. "How much is the limit given to me?" When Li Ming wanted to borrow money, this curiosity became even stronger.

This was already his third "confrontation" with online loans.

In 2019, as a college freshman, Li Ming first came into contact with Huabei, becoming one of the 500 million credit users Alipay claimed that year, overdrawing over 1,000 yuan in a single month. Then came the pandemic lockdown; he was stuck at home, food delivery and online shopping stopped, and he lost the excuse to ask his parents for money, experiencing his first "overdue" payment in his life. After the lockdown was lifted and he returned to school, he got his living expenses and immediately paid off the money, resolutely turned off Huabei, and never used it again.

In 2022, he was a junior. During a routine food delivery purchase, Meituan set "Monthly Pay" as the default payment method; he completed the payment without noticing, and a pop-up immediately appeared, informing him that he had activated this credit product. This was the online loan entrance he encountered most often; Douyin Monthly Pay and JD Baitiao were no different, setting credit products as the default payment method, and he had to be careful not to click wrong every time.

He didn't order much food delivery, only a monthly limit of two to three hundred yuan, but fearing he would develop a habit of超前消费 (overspending), he turned off Meituan Monthly Pay after two or three months.

But what Li Ming didn't know was that to make users like him willingly hand over that one click—pressing the "Check Limit" login button—Zhang Yang, 2,000 kilometers away, had struggled over it for half a year in a tech giant's cubicle.

Zhang Yang is more than 10 years older than Li Ming. This product manager for the online loan business of a tech giant loves pondering literature and psychology and even casually obtained a psychological counselor certificate. His daily job is to adjust the pages of online loan products, battling users' hesitation in milliseconds.

The contest begins the moment Li Ming enters the product page.

"Login" is the step with the highest churn rate; Zhang Yang said 80% of users give up here. And every new user they acquire costs about 500 yuan in advertising fees. To retain them, the team had to try every possible means.

"Login," "Log in immediately," "Give it a try," "Quickly check limit"—"every phrase we could think of was put up." Zhang Yang smiled and shook his head; his computer was full of test documents. For the first screen users saw when opening the App, he tested over a hundred styles in half a month, with twenty to thirty versions competing simultaneously—these pages with only one or two subtle differences were pushed simultaneously to two or three thousand novice users like Li Ming: some saw "Give it a try," some saw "Check limit"...

Then, sitting in front of his computer, Zhang Yang stared at the user click-through rate curve like watching the stock market. Ultimately, the four words "Check Limit" won among all versions. When the change just went live, the proportion of users clicking that button to log in increased by 7%.

This hides the intricacies of psychology. With a hint of pride in his tone, he explained that replacing the word "Login" with "Check Limit" quietly accomplished two things: first, it let the user know clearly what the next step was, eliminating the unknown; second, it reduced the decision-making cost, arousing a person's curiosity about how much they are worth.

To make this "temptation" more attractive, Zhang Yang's team even tested red, white, and blue versions for the text background color, and ultimately blue won. The user conversion rate improvement brought by color tweaking was at most 0.1%, but in front of millions of users, that meant an extra 1,000 Li Mings. If each person borrows 10,000 yuan, at a 3% profit margin, that easily makes an extra 300,000 yuan. Zhang Yang joked, "This is enough for the boss to treat the whole team to milk tea."

And this is just one part. Previously, logging into an App required entering a phone number and waiting for a verification code; these three seconds of blank time were enough for a hesitant person to quit. Now, some online loan platforms directly partner with the three major telecom operators to achieve one-click password-free login, allowing users to skip that time of hesitation.

The core of this set of ideas is very simple: optimize information display, simplify the process, and make it easier for people to complete the action. Such a "brilliant move" quickly became an industry consensus, and similar buttons became popular across major platforms.

Thus, when Li Ming casually pressed that blue button on that sultry afternoon, he thought he was just "looking at a number"; as for what followed the number, he didn't have time to think.

"Ding—" the phone vibrated, 1,000 yuan entered his bank account, taking less than five minutes in total. The moment the bank notification SMS popped up, a trace of pleasant surprise flashed through Li Ming's heart: too fast.

He completely didn't understand what an annualized interest rate was, even though the number exceeded 20%. He only calculated the simplest math: out of the 43,500 yuan limit, he only took 1,000, repaid in 12 installments, paying back a little over a hundred each month. Compared to his monthly living expenses of 2,000 yuan, this was nothing more than skipping a few takeout meals.

But in exchange came an immediate, immense thrill. He immediately had money to buy the music festival ticket; the sound waves thrilled him to the core, and when paying for a late-night snack after the show, he didn't need to hesitate.

But what must come will come. From that afternoon in May 2023, his phone became restless. Online loan SMS messages and calls poured in almost daily, and Du Xiaoman's pop-ups jumped out every week or two to remind him: there is still 42,500 yuan of unused limit.

At that time, he was holed up in a library near his home preparing for the postgraduate entrance exam; every vibration of his phone was exceptionally piercing. Watching his classmates gradually securing jobs, the days of exam prep became even more unbearable. A month later, Li Ming borrowed a second sum on Du Xiaoman, again 1,000 yuan.

As for what he bought, he could no longer remember clearly. He only recalled a莫名 (inexplicable) sense of confidence rising in his heart at the time: since there is a "dream backup fund," why not spend it?

In fact, to make Li Ming return to the platform more often, Zhang Yang and his team put a lot of thought into it.

On the other end connected by the screen, in the backend of online loan product design, users like Li Ming are broken down into various tags by algorithms, and the platform pushes different content accordingly. Zhang Yang gave an example: middle-aged people see rigid-demand ads like "signing kids up for classes" or "renovating a new house," while young people like Li Ming see sentences like "Time to get your girlfriend a new iPhone" or "Apply for a dream backup fund," every word stabbing right at the soft spot of "having no money but wanting to save face."

Just poking at sore spots isn't enough; Zhang Yang's team would also hand out "coupons," attempting to pry open the psychological defenses of those who are starting to get interested in loans.

"As long as we can earn it back from this person, we can issue coupons of any amount." Multiple people who have worked at tech giants like JD Baitiao, Douyin Monthly Pay, and Du Xiaoman told Phoenix Net that to impress users, you have to issue coupons—if 5 yuan doesn't impress, change it to 10, 15, adding them one by one, repeatedly testing until the user is tempted, with the highest going up to over a hundred yuan.

There are also many varieties of coupons: first 30 days interest-free, interest rate coupons, interest and fee discount coupons. "Testing back and forth, there will always be one that hits the mark," they said, their tones as bland as if they were chatting about the weather.

The magic of coupons seems even more hidden than imagined.

Li Ming said that the first time he saw a coupon, he wouldn't immediately want to use it, but it would take root in his mind. When he wanted to spend money someday, this impression would turn into the thought of borrowing. Especially later on, when borrowing became a life habit, the words "three months interest-free" seemed like a bargain picked up for nothing, giving him the illusion: borrowing money is saving money.

Zhang Yang was not surprised by this psychological fluctuation of Li Ming; he said that to attract users at this stage, "all of the seven deadly sins of human nature are being used."

Issuing coupons is to arouse "greed," making people feel that not claiming it is a loss. To provoke "vanity," the ad copy tells you "it's time to get your girlfriend a new iPhone," packaging borrowing as "boyfriend power."

There are also "limited-time interest subsidies" and "8,000 yuan temporary limit, expires in 30 days," which utilize the psychology of "loss aversion": the money didn't belong to you originally, but seeing something about to be in your hands slip away makes people anxious to grab it. Add prompts like "1,000 people have borrowed" and "only three orders left," stimulating herd mentality and dispelling concerns that "borrowing online loans is bad."

All of the above are still considered mild methods.

Zhang Yang introduced that the platform considers the ideal scenario to be having users borrow money here and spend it here. Even if the platform explicitly reminds users that consumer loans cannot be used for investment and wealth management, he said that a small loan company once used a wild tactic: attracting you to borrow with a low 3% interest rate on one hand, while encouraging you to buy a high-risk fund with a 10% annualized return on the other; offsetting interest and returns, it looked like an easy seven or eight points of profit. Many people didn't understand and actually bought it. As a result, the fund dropped, the borrowed money couldn't be repaid, and they were trapped on both ends.

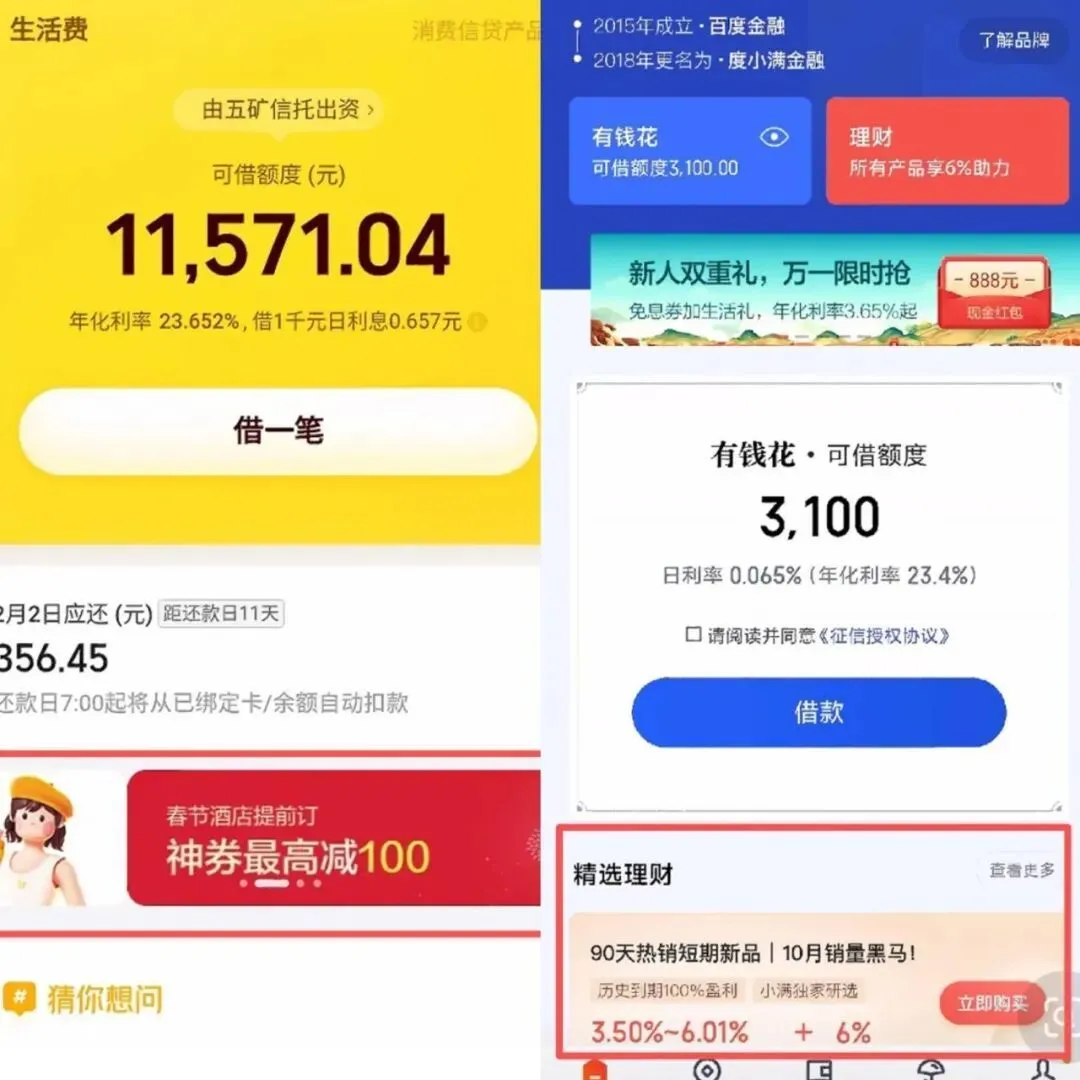

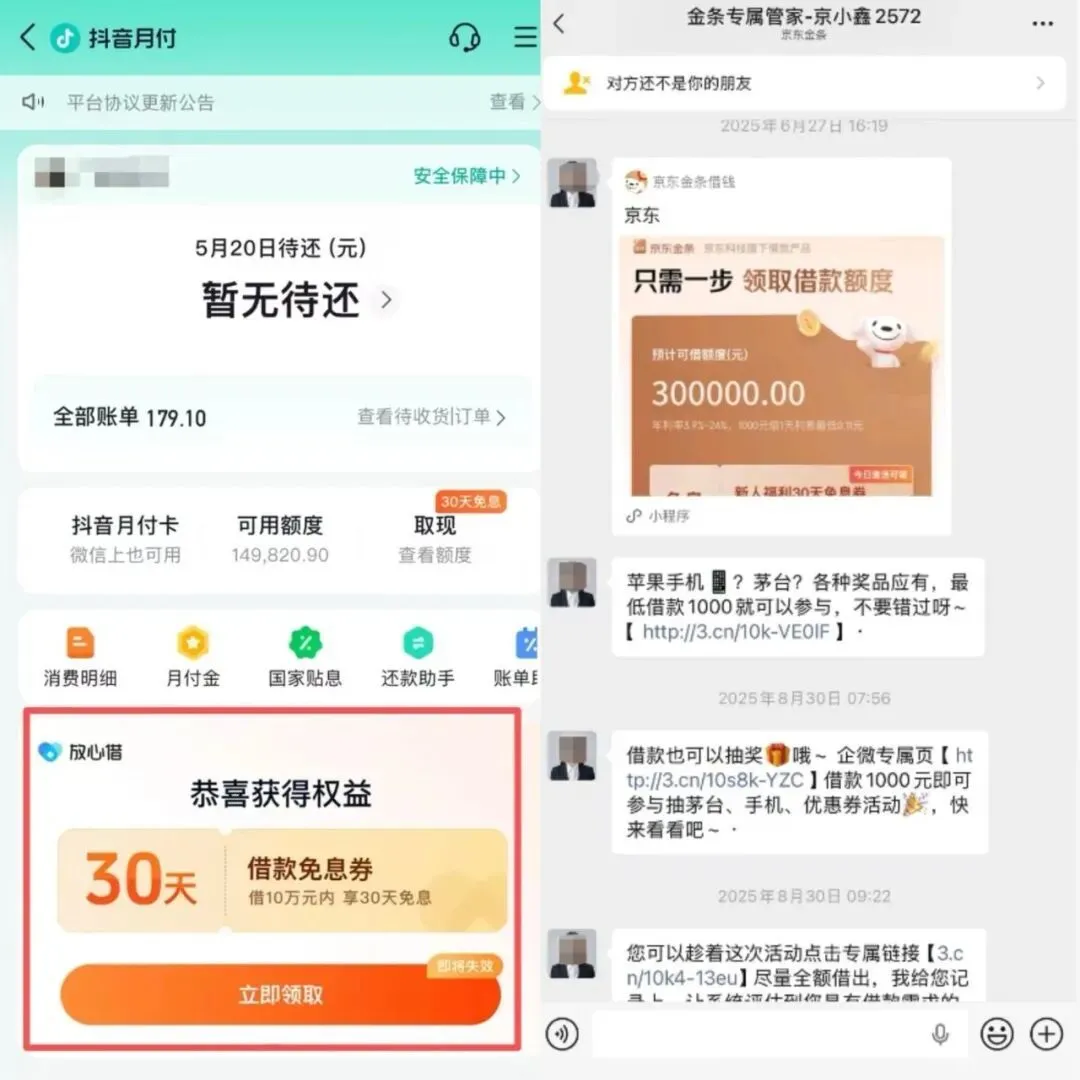

He also said that internet giants wouldn't be so "blatant"; they only stuff wealth management ads and issue consumer coupons on the borrowing page. For example, under the borrowable limit, Du Xiaoman once recommended "selected wealth management" products; under the available limit of Meituan Borrow, it recommended hotel early-booking coupons. "A more hidden approach is to wait until the user has borrowed the money, and then recommend wealth management products via phone calls or text messages."

◎ On the lending pages of Meituan and Du Xiaoman, there were once hotel early-booking coupons and wealth management product recommendations, respectively

Li Ming didn't understand wealth management; he just wanted to spend freely. Once, he opened Taobao and bought three CDs and three vinyl records in one go, spending 2,000 yuan. When his favorite band came to perform in his city, he bought a ticket without hesitation. This exquisite life was all posted on his WeChat Moments, feeding his vanity. The frequency of borrowing got higher and higher, from once every two months to once every half month, and then once every two or three days.

Occasionally, he would feel a bit guilty: was he spending too fiercely? Every ad on his phone seemed to hint that this was accessible freedom; he couldn't stop.

Four months later, Li Ming had cumulatively borrowed 20,000 yuan in online loans, to be repaid in 12 installments. On Du Xiaoman, the monthly repayment rose from the initial 100 yuan to over 2,000 yuan. For someone studying full-time for an exam with no source of income, this money became a monthly "death warrant"; whenever the repayment date approached, he would be too anxious to sleep, his mind full of "what if I can't pay it back?" Borrow from friends? Too hard to ask, not to mention owing a favor, but the key was he didn't want to mention to anyone that he had taken out online loans.

The "way out" had already actively come knocking. His phone had long become a gathering place for ads from various loan apps. "Borrow from another platform to pay it back?" When this thought popped up, he felt quite smart. Among them, the bombardment from "Anyi Hua" was the densest. He scrolled through Xiaohongshu, saw claims of "big platform, fast disbursement," and casually downloaded it. He borrowed 2,000 yuan in the first instance, and transferred it straight into his Du Xiaoman debt. Then came Meituan Borrow, Baixing Bank, and four other platforms, robbing Peter to pay Paul.

At this point, the purpose of the consumer loan had gone beyond consumption; even though the platforms mentioned in some ads and terms that it "cannot be used for repayment," Li Ming was completely trapped in the cycle of "borrowing new to pay old."

A financial industry insider once described this common phenomenon: many existing online loans are not used to expand consumption, but to "prolong the life" of borrowers' cash flows, keeping the debt chain from breaking, especially for flexible workers, the unemployed, and those whose small businesses have failed.

A report by iResearch also showed, based on a survey of 5,285 people, that users who borrow new to repay old and those making large purchases are the deep users of online loan products.

Li Ming also became such a deep user. He used the "tripartite personality structure" in psychoanalysis to explain his behavioral pattern: in reality, he is constrained by the superego (moral constraints); entering the online loan world, he felt a kind of freedom to dominate himself. But soon, desire turned from guest to host, and the id (primal desire) took control of him.

In June 2024, a year after borrowing online, it was the darkest summer of Li Ming's life.

He failed the postgraduate entrance exam, and his debt snowballed to 90,000 yuan. He searched through all the online loan ad links in his text messages, but all he got were rejections. He couldn't sleep at night; scrolling to the SMS reminders of approaching repayments, he thought about suicide.

He wanted to write suicide notes to his parents and best friend, confessing that he owed online loans, "Actually, I'm not the great person you think I am."

Seeing that he was about to default the next day, after tossing and turning, Li Ming finally told his parents. There was no expected storm; they just asked him to explain the debt situation in detail. Then, he worked part-time during the day to earn money and studied for his second attempt at the postgraduate exam at night; the whole family paid off 6,000 yuan in debt together every month. In March 2025, Li Ming passed the postgraduate exam, paid off the last debt, and uninstalled all online loan apps.

He thought that ahead of him was a bright future.

However, six months later, his total debt rolled to 160,000 yuan.

For someone who had easily obtained thrills from "borrowed money," desire doesn't disappear so easily. The online world he lived in hadn't changed—online loan ads still surrounded him.

Tired from studying, he would scroll through Xiaohongshu and catch a glimpse of loan ad posts. On his way home from a part-time job, he'd play a WeChat mini-program game; reviving a character required watching an ad, which was also an online loan ad. He even had a feeling: could it be that because he paid off the money on time, he was instead identified by the system as a high-quality user, and the online loan ads came even more aggressively?

In April 2025, a friend suggested a trip. He remembered taking a ride a month earlier when Didi popped up a window: "You have a maximum limit of 200,000 yuan waiting to be withdrawn"; he hadn't paid much attention then. Now, a thought revived: just this once, for an emergency. So, he borrowed 5,000 yuan on Didi, repaid in 12 installments, paying over 500 yuan a month, exactly one-tenth of his salary at the time.

For people like Li Ming, breaking their resolution again is not an isolated case.

Another 25-year-old young man had a similar trajectory. His family had just helped him pay off an 80,000 yuan debt, and the following year he restarted online loans, owing 100,000 yuan. He told Phoenix Net that he was confused himself, "Should we blame ourselves for not being able to control it, or are online loans just too easy?"

A person who owed 1 million yuan in online loans recalled to Phoenix Net that over a period of more than a month in 2024, he took screenshots of the loan ads pushed to his WeChat Moments every day—Weili Dai, 360 IOU, Ctrip Finance... an average of three a day, piecing together a long image of over a hundred screenshots. Staring at that picture, he just felt "furious." He believed that if it weren't so easy to borrow money, he wouldn't have ended up like this.

◎ 1 million yuan in online loan debt; screenshots of loan ads in WeChat Moments recorded over more than a month

Online loan ads are like internet "psoriasis," surrounding all ordinary people who touch the internet, and this, too, is meticulously designed.

First is the "hard attack" at the algorithm level.

Feng Yongqiang works in ad placement for an online loan company; most of the company's ad budget is poured into the information streams of Tencent and ByteDance. He calls people like Li Ming who "used online loans but stopped" the "offline crowd package." Their behavioral traits are broken down into data tags and passed to Tencent and ByteDance, which will "build models" based on them—the platforms' technology for screening crowds, used to precisely fish out potential online loan users with similar characteristics from the sea of people.

At this stage, the core resource for Feng Yongqiang and his team is the potential users' phone "device IDs." The reason it's not the users' phone numbers is that it easily crosses the policy red line of privacy protection. As long as any app is downloaded, the front end has the opportunity to collect the other party's phone device ID; online loan companies can find third parties to obtain every user's behavioral data on the app through the device ID, figuring out their consumption and repayment capabilities.

After locking onto the targets, the next step is information "bombardment." To achieve "saturated penetration" of ads, Feng Yongqiang's strategy is to concentrate placements on the three peak periods of morning, noon, and evening; for the same user, the ad is exposed over 10 times by default. At the same time, the ad copy materials "can iterate from dozens to over a hundred in a week."

Second is the "soft persistence" of various posts on social media.

Wang Qingyue was once the marketing head of a lending platform. He recruited college students as writers through a club at a 211 university in Beijing to post image-and-text notes on Xiaohongshu, paying 15 to 20 yuan per post, with only one requirement: "No hard ads, tell a story."

These notes precisely anchor young people's material desires. For example, "Not enough money to buy a phone, write an IOU and take it away"; the content specifically targets the pain points of people short on money. Besides using student accounts for volume, the company also has cooperating lawyers, using the professional image of lawyer accounts to give the product legal credibility. Wang Qingyue once did a user survey; this self-media traffic method contributed 30% of the company's new borrowers.

But Wang Qingyue was more envious of the tech giants; without racking their brains to find people to post promotions, their online loan products could be embedded in most consumption scenarios for traffic diversion, and users naturally trusted them: when topping up phone credit on WeChat, a Weili Dai coupon lies right there; ordering food on Meituan, watching live streams on Douyin, or shopping on JD, the system all defaults to checking "Baitiao" or "Monthly Pay."

"The user's default payment is JD Baitiao; since I joined, as far as I can remember, it has almost never changed," said a person who once worked at JD Baitiao, noting that even if this affected user experience, no one internally ever suggested adjusting it.

Wu Chaodong, who previously worked at Douyin Monthly Pay, mentioned, "For 20% of transaction users, the platform will default check Douyin Monthly Pay, and the next payment method will also default to Douyin Monthly Pay."

This is because users who "accidentally" used Baitiao and Monthly Pay are exactly the group online loan products crave the most. "Their overdue rate is only one-tenth that of users who actively come to borrow money," Wu Chaodong said.

He introduced that the trick hidden here is the platform's common tactic of switching users from "left hand to right hand," converting ordinary users into online loan users. "You're scrolling through short videos on Douyin, casually buying a small item, defaulted to Douyin Monthly Pay; once you use it, you always have to come back to repay the money, right?" Once on the repayment page, the ad for Douyin's cash loan product "Fangxin Jie" rushes at you—golden background, bold font: "Congratulations on obtaining the privilege, 30-day interest-free loan."

It wasn't until recent regulatory intervention that the default checking and front-end recommendations of Huabei and Baitiao will face adjustments in October 2026.

It was in this online environment that Li Ming, just from taking a ride, started using online loan products again. He said that among the many online loan ads bombarding him, the reason for choosing Didi Borrow was simple: "big platform."

The "fierce beast" had already been released. In the past on Du Xiaoman, Li Ming only borrowed a thousand at a time; but now on Didi, he borrowed ten thousand at a time. He said he felt scared, but his fingers still couldn't stop clicking.

Where did the money go? Food, drinks, travel, buying CDs, and repaying loans. He counted: sixty or seventy CDs, adding up to over thirty thousand yuan. What's hard to explain is that, apart from satisfying vanity just like posting travel photos, none of these things were what he truly needed.

But the stakes attracting him were still increasing.

After borrowing on Didi for over a month, one day while resting in his dorm, a text message suddenly popped up: Didi had temporarily raised his limit from 80,000 to 140,000 yuan, expiring in 29 days. He clicked into Didi to check, and it really had gone up, and indeed he could borrow it. This "unexpected joy" also added a bit of a "feeling of being trusted by the platform." A little over a month later, the drama of temporarily raising the limit replayed. By this time, Li Ming "wanted to borrow every three or four days."

In the eyes of Feng Yuekai, an online loan risk control manager at a tech giant, this is completely normal. Once a user clicks to authorize credit checking, they are almost naked in the eyes of the backend system. Doing risk control, as long as he "lets a little water slip," he can raise the approval rate of loan applicants' qualifications from 30% to 35%, which for the company means "solid growth in loan scale and profits"; this is much more efficient than Zhang Yang's method of polishing user login pages for acquisition.

In Feng Yuekai's view, a user's credit report is a "reference map" for online loan platforms to adjust lending strategies targetedly. With the same 100,000 yuan limit, "If you only borrow 30,000 here but borrow 100,000 there, it means the interest rate there is more attractive." Feng Yuekai said that for such customers, the platform will proactively raise limits and lower interest rates to attract them over.

This is also why Li Ming experienced two limit increases on Didi. At this stage, Du Xiaoman and Meituan Borrow, where he had borrowed before, were also throwing olive branches at him.

However, just two months after the limit increase, Li Ming quickly became an "abandoned piece." In September 2025, Li Ming returned to campus for his graduate studies, lost his income, and could no longer borrow money on Didi. Having had one online loan experience, he immediately realized he couldn't borrow from other platforms either.

Feng Yuekai said that algorithms can clearly capture his borrowing trajectory across major platforms: repeatedly borrowing across multiple platforms within half a year, even if not yet overdue, is itself a danger signal. Li Ming had already been viewed by the system as "a person no longer worthy of lending to."

However, how to calculate the exact timing of completely withdrawing a user's loan limit—this core question of risk control—Feng Yuekai did not answer.

Wu Chaodong, taking Douyin and JD as examples, explained to Phoenix Net the "funnel game" used by internet giants to judge borrowers' qualifications.

Using Douyin as an example, the platform prioritizes directing users of "Douyin Monthly Pay" to its own product "Fangxin Jie"; users coming from this port can have a loan qualification approval rate as high as 70%, which is 20% higher than those who proactively come to borrow. And the "low-quality users" who fail the loan qualification review are categorized by region and qualification, and diverted to third-party lending institutions—the platform can charge fees for selling traffic, or take a cut of dividends. More crucially, once these users are found to "perform well" on third-party platforms, repaying on time, they will be "fished" back into the platform's own online loan products.

When a person is compressed into "tags," how does the algorithm dismantle, convert, and eventually discard them? Phoenix Net asked multiple industry insiders who had worked at JD Baitiao, Douyin Monthly Pay, and Du Xiaoman; they all shook their heads, saying they "couldn't explain it clearly." Tagging by age, occupation, and city is already outdated. Now, everything is left to the algorithm.

"We only use models now," said Wen Qingsong, a former mid-to-senior executive close to the financial line at Douyin. Truly pondering the causal relationships of user behavior one by one is too inefficient; by the time the analysis is done, the user's habits would have long changed, whereas the model is like a black box stuffed with thousands of variables; as for how it actually calculates, "we don't know, and we don't want to know."

Through the "funnel game," an ordinary person initially using small consumer loans might end up burdened with massive debt within a few years. Li Ming is one of them; another post-90s programmer who eventually owed 600,000 yuan told Phoenix Net that he initially just bought a 20,000 yuan computer using JD Baitiao in 2022, repaying in 12 installments, nearly 2,000 a month. He took home 25,000 a month, so there shouldn't have been any pressure, but all the money was controlled by his wife; he could only rely on playing "Fantasy Westward Journey" and selling some equipment to scrape together money for repayment.

At first, he barely managed, but by the 7th installment, he couldn't pay. At this time, he received a promotional text message recommending he download the JD Finance app, and a customer service rep added him on enterprise WeChat, recommending he use JD Jintiao (similar to Alipay's Jiebei). He realized he could use JD Jintiao to borrow money to repay JD Baitiao. So he borrowed to repay, repaid to borrow, cycling over and over. Until one day, clicking into the familiar JD Finance link, he was told his qualifications didn't meet the criteria, and the page automatically redirected to a third-party lending platform, where the interest rate, plus guarantee fees, approached 36%.

On January 1, 2026, he confessed everything to his wife. While he was deeply trapped in the debt vortex, JD Jintiao's customer service was still sending him messages via enterprise WeChat: "Borrowing money also gets you a lottery draw~"

◎ "Fangxin Jie" under Douyin Monthly Pay; JD Jintiao customer service sending loan information via enterprise WeChat

"How could someone mess up their life twice?" With debt pressing down on him again, Li Ming was utterly disappointed in himself.

This time it was 160,000 yuan, and he didn't want his parents to know. He looked for part-time work, posting ad comments as a paid troll, earning 3,000 a month, but his monthly loan repayments were six or seven thousand; he couldn't find a more lucrative path.

At this point, he could only blame his own excessive vanity. Recalling his college graduation, it coincided with the end of pandemic lockdowns; jobs were hard to find, but at the same time, on the internet, there were "show-off posts" of glamorous lives everywhere, and he wanted to live like that too. The online loans surrounding him told him: just borrow, this is the easiest path.

Separated by a screen, online loan designers don't individually interact with people like Li Ming. An ordinary person's overdue rate, customer acquisition cost, re-borrowing rate, and lifetime value are all quantified into numbers.

But one thing is certain: the designers have a very clear understanding of a person's debt-bearing capacity. Wen Qingsong said that a person who repeatedly uses a platform for four years definitely has financial problems; Wang Qingyue said that once a person's online loan amount exceeds 25 times their annual income, it's very hard to turn things around.

They operate within a well-functioning system, completing their assigned tasks.

Working for tech giants, they build their own decent lives. Working in bright places, everyone is young, well-dressed, and walking briskly.

Working for tech giants, the designers also feel exhausted. Zhang Yang is most annoyed by online loan product updates and launches, always having to stay up late, his heart occasionally aching. The pressure is also immense; the KPI of converting more users into online loan customers has to double every year. He said he was tired of it and couldn't endure the grind anymore. As for the moral pressure of doing this job, there is none: "I'm not running a porn site."

These efforts ultimately transform into the flashy financial numbers of large corporations. Ant Consumer Finance had a net profit of 3.1 billion yuan in 2025, earning about 8.52 million yuan a day. In 2024, Du Xiaoman earned a net profit of 859 million yuan a year, 2.35 million yuan a day, and its consumer loan non-performing rate was only 1.09%, far below the industry average of 1.97% in the same period.

"Only an idiot wouldn't make money when it's there." Wang Qingyue blurted out; in short, this is the easiest business to make money, so why not make it. It is a consensus that internet giants are inherently equipped with the DNA to make lending products.

Wen Qingsong said that whenever a company grows large, the first thing it does is create its own payment channel; one, it can save the channel fees that would otherwise be paid to WeChat and Alipay; two, it can hide the platform's real transaction data, preventing third parties from seeing through its bottom line. And once payment is established, credit business logically derives—users spending money in these app scenarios will generate the need of "what if I don't have enough money"; rather than letting users jump to other platforms to borrow, it's better to conveniently lend them the money yourself, earning an extra income and boosting the platform's transaction volume.

This money-making logic is expanding infinitely. On the Black Cat Complaint platform, the number of complaints involving Ant Financial, Du Xiaoman, JD Baitiao, and Meituan Borrow are 32,000, 45,000, 83,000, and 328,000 respectively, with a large number of complaints involving debt collection and high interest rates.

Following this are wave after wave of strictest regulations; the lending space with interest rates originally between 24%-36% in the industry is required to shrink, and at the same time, the chaos of internet giants making users default check "Monthly Pay" at payment time has also been given a red line.

◎ Complaints about Ant Financial, Du Xiaoman, JD Baitiao, and Meituan Borrow on Black Cat Complaints

It's just that the internet algorithm system surrounding Li Ming is still operating as usual. Here, everything is compliant, yet he still fell into the abyss.

The online loan world Wang Qingyue sees is stratified. The first layer is bank users, the second is internet giant users, the third is small loan company users, and the fourth is users trapped in the abyss of usury. Users seep downward through the layers of filters like residue. The further down, the worse the "quality." The company he once served did business with people in the fourth layer.

Once for work needs, he pulled up a batch of IOU attachments uploaded by users. To his surprise, there were girls' nude loans among them. Sitting in the office, he subconsciously closed that window, but the image was already branded into his mind: a cheap rental apartment bathroom background, a girl in her early twenties, long hair draped over her shoulders, holding her ID card, eyes empty; the amount she borrowed was only one thousand yuan.

"What made her need to do this?" This thought lingered in Wang Qingyue's mind for a while; he was puzzled that a young person who should have had a future would seep from the first layer to the fourth so early.

Such stories of descent are constantly repeating in corners unknown to people.

Sometimes, Feng Yongqiang gets curious about the people behind the numbers; he sees people willing to bear high interest rates for a few hundred yuan, "Why do they still borrow?"

In his friends' eyes, Li Ming is still that "high-quality youth" who is knowledgeable, calm, and loves collecting records. But only he knows clearly that under precise algorithms, having overdrawn his last limit, he has fallen from a "high-quality customer" to "data dust."

For a long time, he locked himself in his room, casually playing a video as background noise, and began mechanically swiping his finger on Xiaohongshu. The screen was crammed with all sorts of "shady" solutions; he told himself "this must be a scam" while simultaneously unable to resist clicking in—what if it's useful?

He had studied addiction mechanisms; once a person is immersed and the satisfaction is intense, it overrides rationality, just like people sitting in a casino who initially just went to play.

Suicidal thoughts once again surfaced in Li Ming's mind. What he feared wasn't just that this 160,000 yuan couldn't be paid off. He was even more terrified that, if he lived, would he make the same mistake again in the future.

Everything started with "Check Limit." But exactly from which day onward his life could never go back, no one could answer him.

As requested by the interviewees, Li Ming, Zhang Yang, Feng Yuekai, Feng Yongqiang, Wang Qingyue, Wen Qingsong, and Wu Chaodong are all pseudonyms in the text.

Author Li Qiuhan | Editor Yan Qing

微信扫一扫打赏

微信扫一扫打赏  支付宝扫一扫打赏

支付宝扫一扫打赏

Comments (0)