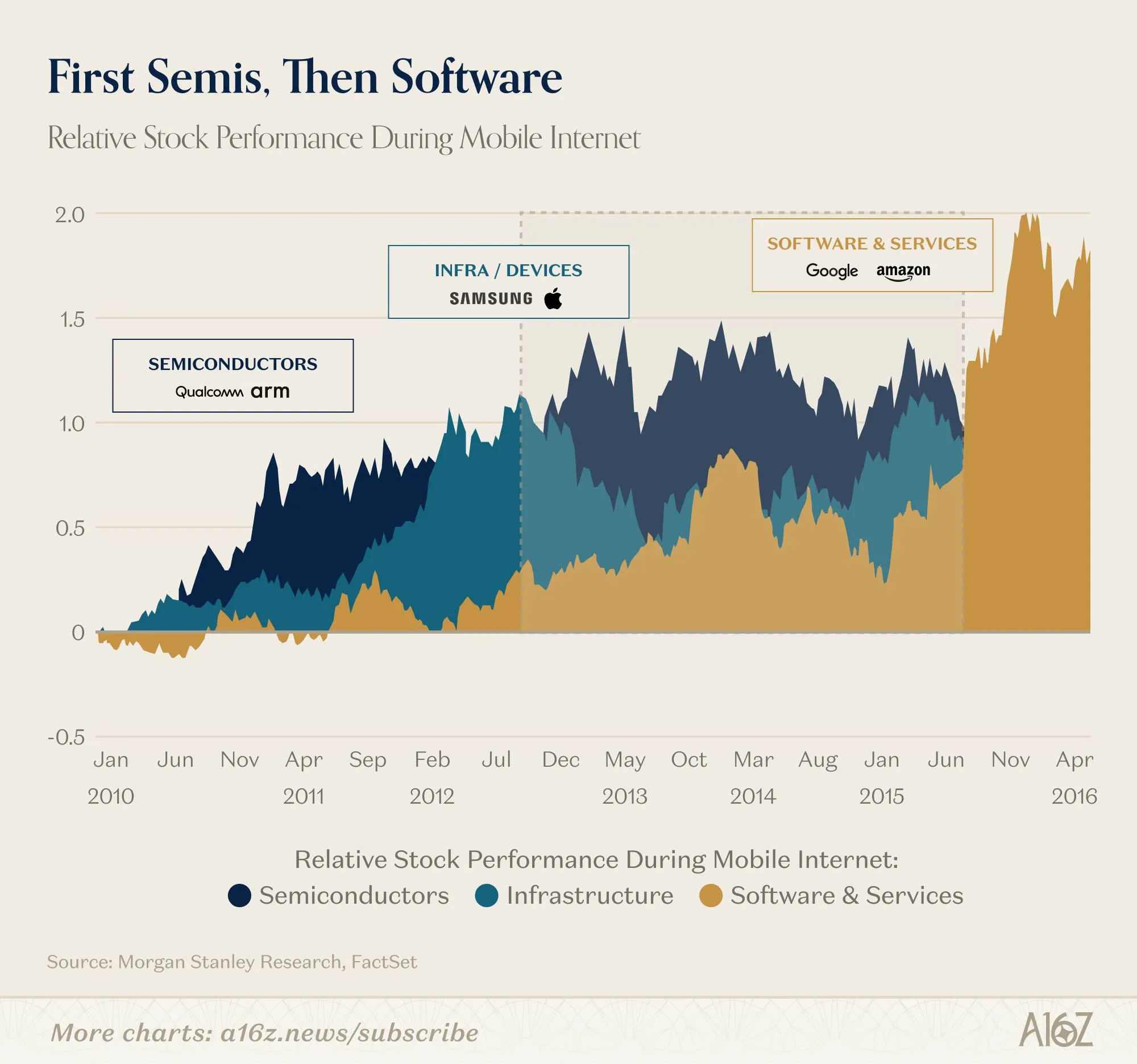

@有限次重复博弈:This chart reviews the relative stock performance during the mobile internet era. The most interesting part is that market dividends were not simultaneously granted to all tech companies; instead, they transmitted upward along the industry stack. The first to benefit were semiconductors, followed by devices and infrastructure, and finally software and services.

During the period from 2010 to 2012, the first to stand out were chip companies like Qualcomm and ARM. The reason is straightforward: before every smartphone could be born, the first things needed were processors, communication chips, and underlying hardware—those selling the shovels naturally started making money first.

Next came the turn of platform and device companies like Samsung and Apple to benefit. When mobile phones began to gain mass adoption, the companies that truly integrated hardware into consumer products and put them into everyone's hands took the baton to become the market focus, capturing the dividends of the device普及 stage.

But ultimately, those who won the longest and reaped the most were the software and services layers. When hardware was already widespread and users were online, value would gradually concentrate toward the application side. Google, Amazon, and even the entire app ecosystem eventually moved to the forefront, because traffic, usage time, and monetization all happened there.

Applying this sequence to today's AI cycle, it easily reminds people of the current market landscape. Right now, the strongest are semiconductors, data centers, servers, and infrastructure, because computing power is still in a period of massive expansion. But if history is any guide, then the software layer, which can truly transform AI into everyday tools and business models, may very well become the protagonist of the next stage.

微信扫一扫打赏

微信扫一扫打赏  支付宝扫一扫打赏

支付宝扫一扫打赏

Comments (0)